The allocation of additional material assistance to an employee by an enterprise is a fairly common phenomenon. Therefore, 1C:ZUP provides for the possibility of accounting for financial assistance in connection with the appearance of a child, marriage, for study leave or illness, as well as accounting for accruals to a former employee.

By decision of the general meeting of the founders of the organization, the amount of material assistance payments may be included in net profit, or be added to other expenses.

According to paragraph 23 of Art. 270 of the Tax Code of the Russian Federation, the amount of material assistance included in other expenses refers to expenses that are not taken into account for income tax purposes. Therefore, if the company decided to provide material assistance from retained earnings, then the posting will be carried out on account 84, otherwise account 91.02 is used, and these are other expenses.

As an example, let's look at how to reflect in the software solution "1C: Payroll and Personnel Management" ed. 3.1. reflection of material assistance allocated to a retired former employee Mamontova A.V.

Mamontova A.V. was provided financial assistance in the amount of 20,000 rubles, since she underwent a surgical operation. Let's pay attention to the fact that earlier this year, financial assistance to employees who had already left the enterprise was not allocated.

Setting up 1C: ZUP 3.1

In order for the program to be able to accrue financial assistance, go to the payroll settings and activate the parameter for paying income to former employees of the enterprise:

Menu "Settings"->Payroll

It should be noted that financial assistance is subject to personal income tax and insurance premiums in different ways. Therefore, it is necessary to set up the directory "Types of payments to former employees":

Menu "Payouts"->See. See also->Types of payments to former employees

To set up payments to employees of the enterprise dismissed due to the onset of pensions, as well as reimbursement of the cost of medicines to disabled people, select the appropriate type of payment predefined in the program.

*Note that in the case of assistance to a previously dismissed, but not retired, employee, the payment of financial assistance will be made with the deduction of personal income tax in the amount of 13%.

Registration of payment of financial assistance

The next step is to register for help. To do this, you must use the document "Payment to former employees", designed to fix the amount of personal income tax and/or insurance premiums, and further reflect them in the reporting, including the regulatory one.

Menu "Payments"->Payments to former employees

We create a new document. We will give explanations on the introduction of details in the document, which usually cause doubts:

- Month - the exact month of registration of material assistance in the program is indicated;

- Type of payment - the guide "Types of payments ..." will help determine the type of payment. If the option you select includes an additional withholding of taxes or contributions, fields such as Personal Income Tax Code, Insurance Contributions, and Deduction will be filled in automatically;

- Payment date - During the document, all transactions with personal income tax are fixed by the date indicated in this field;

- When adding a former employee to the tabular section, a form with a limited selection of employees will open, in which only those persons who have already received payments or those who previously worked for the company will appear. If an employee left the enterprise before the start of accounting in the program, he should simply be added to this list. This is done through the selection window:

- Accrued - the amount of financial assistance;

- Deduction amount - income deduction amount, where personal income tax and insurance premiums are calculated automatically;

- Personal income tax - data on retention are reflected. Here you can also see information on the calculation of NFDL;

- To be paid - the final figure of financial assistance;

- Contributions - reflects the amount of accrued insurance premiums.

*Recall that insurance premiums are subject to payments under labor and civil law contracts providing for the performance of work, as well as the provision of services (part 1 of article 7 of the Federal Law of July 24, 2009 No. 212-FZ and paragraph 1 of article 20.1 of the Federal Law of July 24 .98 No. 125-FZ).

This document also provides a printed form, it looks like this:

Analysis

Get comprehensive information and analyze payments to former employees will help the report "Unsalary income"

Menu "Payouts"->Reports on payments

To accrue financial assistance to employees in 1C ZUP 3.1, set up the payroll calculation, if necessary, you can customize or create types of calculation for accrual and register material assistance either in the document Material aid , or a document Vacation(if you need to accrue financial assistance for vacation).

To accrue financial assistance to former employees, a document is used Payment to former employees .

Financial assistance in the general case (except for financial assistance for vacation)

Setting up 1C ZUP 3.1 for calculating material assistance

In the payroll settings, check the box ():

As a result of checking the box, three types of accrual will be added with the purpose Material aid :

Each of these types of accrual has its own taxation settings and is used for registration various kinds financial assistance:

If necessary, copying on the basis of these types of calculation, you can create new types of accrual, if, for example, it is customary for an organization to divide material assistance not only by taxation methods, but also for some other reason, for example, according to the method of reflection in accounting. The main thing is that the purpose is indicated in the accrual type settings Material aid and performed According to a separate document :

Using the Document "Material Assistance"

Calculation of financial assistance in 1C ZUP 8.3 in the general case (except for financial assistance for vacation), complete in the document Material aid , which becomes available after the checkbox is checked Financial assistance paid to employees in payroll settings.

In document:

When registering financial assistance by code personal income tax 2760 (by default, this is the type of accrual Material aid ) the deduction is applied 503 in the maximum amount of 4,000 rubles. Since 4,000 rubles. - this is the amount of the annual deduction for material assistance, then in the 1C ZUP 3.1 program it is tracked what amount by the deduction code 503 was applied to each of the employees in the current calendar year.

For Financial assistance at the birth of a child (personal income tax code 2762 ) in the document it is important to indicate Amount of children for the deduction to be applied 508 :

Payment of financial assistance

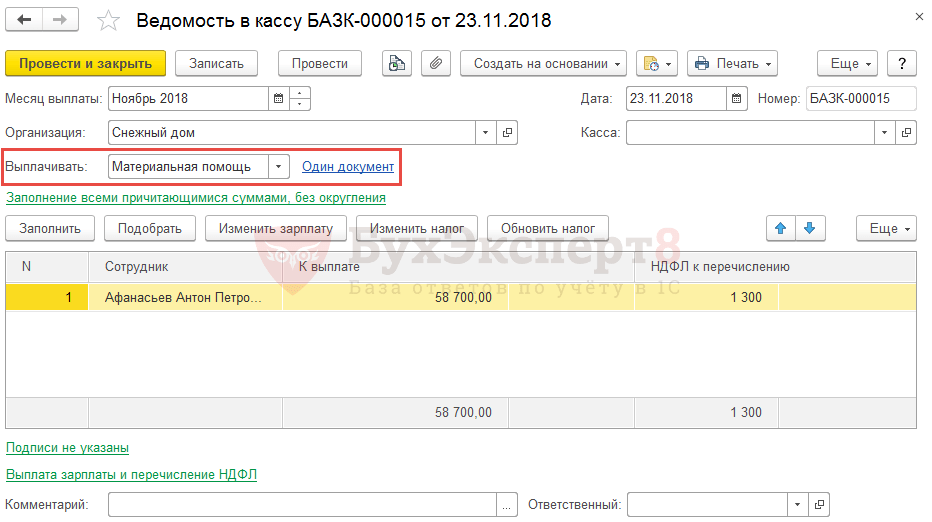

In the case of payment of material assistance in the inter-settlement period, payment in 1C ZUP 3.1 can be registered directly from the document Material aid on command pay out .

As a result, a document will be created Vedomosti… with payment method Material aid and referring to this document Material aid .

Also, a statement can be created independently, directly from the journal of statements, specifying the method of payment Material aid and selecting the documents for which the payment is made.

To accrue financial assistance for vacation in 1C ZUP 3.1, in the payroll settings, check the box Financial assistance for vacation (Settings - Payroll - Setting up the composition of accruals and deductions - Material assistance tab):

As a result of checking the box, the accrual type will appear Financial assistance for vacation . By default, for the type of accrual, the formula for calculating the amount of a multiple of the salary is defined (the multiplicity is set during the initial setup of the program). You can edit the formula if necessary.

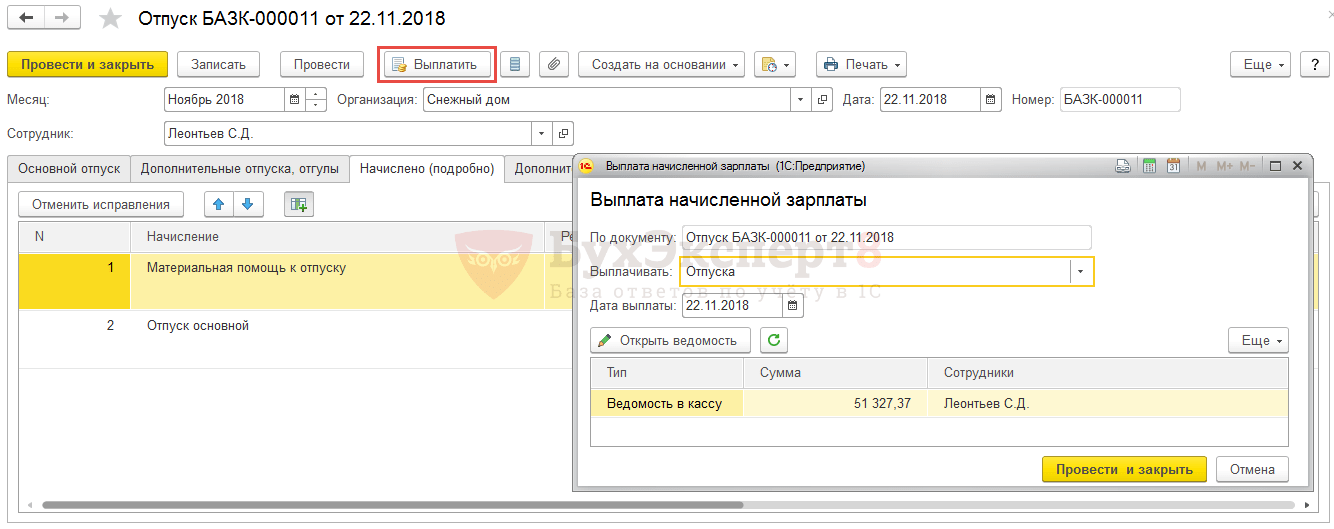

Accrual of financial assistance for vacation in 1C ZUP 3.1 reflect the document Vacation. To calculate such material assistance on the main tab, check the box Financial assistance for vacation :

As a result, on the tab Accrued (detailed) will be calculated according to the type of accrual Financial assistance for vacation :

The payment of financial assistance for vacation occurs along with vacation pay. The statement can be entered either directly from the document Vacation on command pay out, or in the journal of documents Vedomosti… by specifying the payment method Vacation and the document itself, according to which the payment is made.

Financial assistance to former employees

The employer may also pay financial assistance to former employees. To register such financial assistance in 1C ZUP 3, in the payroll settings, check the box Income paid to former employees of the company .

After that, in the guide Types of payments to former employees define the settings for the material assistance paid: the personal income tax code and the type of insurance premium income. You can describe several types of financial assistance with different settings, if required.

Specify the required type of payment in the document Payments to former employees , select former employees (from the directory Individuals ) and indicate the amount of assistance paid.

Document Payment to former employees in 1C ZUP is used for the purposes of accounting for personal income tax, contributions and generating data in a document Reflection of salary in accounting . Document Vedomosti for the accrual of payments to former employees in the ZUP is not introduced. It is assumed that the settlement with former employees is recorded in the accounting program.

Watch our video tutorial on calculating financial assistance in 1C ZUP 3.1:

An enterprise, at the request of its employee or on its own initiative, can accrue and pay material assistance. In this article, I want to tell you how to do this in 1C ZUP 8.3, in the form of step-by-step instructions.

Financial assistance refers to one-time payments. In previous versions of the 1C ZUP program (8.2), to reflect this type of accrual, there was a document “Registration of one-time accruals for employees of organizations”. Now he is gone. Many people have a question, how to accrue financial assistance? I must say right away that there is such an opportunity, but initially it was disabled in the system.

Program settings 1C ZUP for the accrual of financial assistance

To make the “Material Assistance” document available in 1C ZUP 8.3, you need to make two settings. The first is to check the box "Paid financial assistance to employees."

We go to the settings section of 1C Enterprise (the "Settings" menu, then follow the "Payroll" link to go to the payroll settings). In this window there is another link: "Setting the composition of accruals and deductions." We click on it. Another settings window will open. It contains several bookmarks. We are interested in the "Other accruals" tab. This is where the above checkbox needs to be checked:

Now in the "Salary" section, the menu item "Material assistance" will appear.

The second setting that needs to be done is to add an accrual with the “Material assistance” assignment to the list of accruals.

Get 267 1C video lessons for free:

- On the “Basic” tab, in the “Account purpose” field, select “Material assistance”.

- In the "Accrual in progress" field, specify "According to a separate document".

- In the "Calculation and indicators" section, select the calculation method - a fixed amount.

Basically, this method is used, although it is possible to set a formula for calculation, starting from any indicators. These indicators will appear later in the document for filling out:

Click "Save and Close".

By the way, if you do not go into the settings for the composition of accruals and deductions, but add an accrual with the purpose “Material assistance” to the list of accruals, then the checkbox in the settings will be set by itself, and the menu item will also appear automatically.

Let's start calculating.

Accrual and payment of material assistance in 1C ZUP

By clicking the "Create" button in the form of the "Material Assistance" list, we will create a new document.

Fill in the header of the document. I will pay attention to the props “Type of financial assistance”. Help can be provided for various reasons, so there may be several settings with this purpose. Here we select the calculation we need. Let's add an employee to the table. In the "Result" column, indicate the amount of financial assistance. The deduction code the program prompts us to select "503". When choosing a code, the program should calculate the amount of the deduction for us.

The document has two calculation options:

- automatically;

- manually by clicking the "Recalculate" button.

If the "Automatic calculation in documents" checkbox is not checked in the settings, then a yellow button will appear in the tabular section when changing the details. To recalculate the document, you need to click it.

But here I ran into a problem. In my settings, automatic recalculation was disabled, and to calculate the amount of the deduction, I clicked on the button. The result is like this:

That is, an error occurred, and the amount was not calculated. Perhaps the error has already been fixed in your release of the program, and you will be able to recalculate the amounts without additional settings of the 1s 8.3 program.

Enterprises can provide material assistance to their employees and other individuals. The amount of material assistance is not established in the legislation and is determined by the organization independently.

Based on paragraph 28 of Art. 217 of the Tax Code of the Russian Federation are not subject to personal income tax in an amount not exceeding 4,000 rubles. per year financial assistance, which is provided:

employers to their employees, as well as to their former employees who left due to retirement due to disability or old age;

disabled people by public organizations of disabled people.

In accordance with paragraphs. 3 p. 1 art. 422 of the Tax Code of the Russian Federation, paragraphs. 3 p. 1 art. 20.2 of Federal Law No. 125-FZ of July 24, 1998, lump-sum financial assistance is not subject to insurance premiums if financial assistance is provided:

to individuals to compensate for material damage caused to them or harm to their health in connection with a natural disaster or other emergency circumstance, as well as individuals who suffered from terrorist acts on the territory of the Russian Federation;

an employee in connection with the death of a member (members) of his family;

employees (parents, adoptive parents, guardians) at birth (adoption (adoption) of a child, establishment of guardianship over a child, paid during the first year after birth (adoption (adoption), establishment of guardianship, but not more than 50,000 rubles for each child.

The amounts of other material assistance provided by employers to their employees, on the basis of paragraphs. 11 p. 1 art. 422 of the Tax Code of the Russian Federation are not subject to insurance premiums in an amount not exceeding 4,000 rubles per employee for the billing period.

Accounting for material assistance in 1C Accounting 8 ed. 3.0

Consider accounting for financial assistance in the program using the example of financial assistance for vacation.

Under the terms of the collective agreement, Karavay LLC once a year provides employees with material assistance for annual paid leave in the amount of a monthly salary. In July 2016, an employee of Kremova K.K. leaves for the next annual paid vacation, while he is paid a one-time financial assistance for the vacation. The salary of an employee at the time of granting leave is 25,000 rubles.

For the calculation of financial assistance in the program 1C Accounting 8 ed. 3.0, first we will create a new type of accrual. It can be found

In the name we indicate "Material assistance for vacation."

On the personal income tax line, we indicate code 2760 “Material assistance provided by employers to their employees, as well as to their former employees who quit due to retirement.” Income under this code in the amount of up to 4,000 rubles is not subject to personal income tax during the calendar year.

In our example, financial assistance is provided for the first time in a year.

In the column of insurance premiums, we indicate that material assistance is subject to insurance premiums in part, that is, only the amount over 4,000 rubles will be taxed.

For income tax, this type of material assistance will be taken into account in labor costs and we select paragraph 25, art. 255 of the Tax Code of the Russian Federation.

We do not set the checkbox “Included in the base charges for calculating the charges“ District coefficient ”and“ Northern allowance ”.

The reflection method for financial assistance for vacation can be omitted, because. it will be credited to the same account as the employee's salary. Therefore, the program will take the reflection method either from the general setting, or from the method specified in the employee directory.

For other types of material assistance, which are accrued to 91 accounts and are not included in labor costs, it is necessary to create a new method of accrual Dt 91.02 Kt 70.

For the calculation of material assistance in 1C Accounting 8, the document “Payroll” will be used, located in the “Salary and Personnel”, “All Accruals” section. This accrual is a one-time charge, so information can be entered into the document manually. We select an employee, indicate the type of accrual and the amount. According to the document, personal income tax and contributions will also be calculated.

Postings are generated according to the document:

Financial assistance is cash or other property provided by the employer to its employee in connection with a natural disaster or other emergency, the death of a family member, the birth of a child, vacation or other circumstances.

About what postings for material assistance an employee needs to do in accounting, we will tell in our material.

Determine the type of financial assistance

The accounting procedure for material assistance depends on its type and method of provision.

If financial assistance is a one-time payment to an employee when he is granted annual leave, the payment of such assistance is provided for by the labor, collective agreement or local regulatory act of the employer and is associated with the employee's performance of his labor function (depends on the amount of wages, compliance with labor discipline, etc. ), then such assistance is part of the wage system and is reflected in the general procedure characteristic of.

So, financial assistance for vacation can be accrued with the following accounting entries ():

Debit of accounts 20 “Main production”, 26 “General business expenses”, 44 “Sales expenses”, etc. - Credit of account 70 “Settlements with personnel for wages”

In addition, it is necessary to reflect the withholding of personal income tax and the accrual of insurance premiums, as well as the issuance of financial assistance:

And if the payment of financial assistance is not related to the provision of leave to the employee in accordance with the wage system, its accounting procedure will be different.

Assistance as part of other expenses

Financial aid paid to an employee on other grounds will be reflected as part of other expenses on account 91 “Other income and expenses” (clauses 12, 13 PBU 10/99, Order of the Ministry of Finance dated 10/31/2000 No. 94n):

Help in kind

If material assistance is given to an employee not in money, but in property (for example, goods), then instead of accounts 70 and 73, the accounts of property released as financial assistance will be credited.

In addition, since the transfer of ownership of goods on a gratuitous basis is recognized as a sale, VAT will have to be charged on the market value of the transferred property (clause 1, clause 1, article 146, clause 2, article 154 of the Tax Code of the Russian Federation).

Personal income tax from the amount of natural assistance will need to be withheld from the employee's cash income.